Rooftop PV and battery storage

Key insights

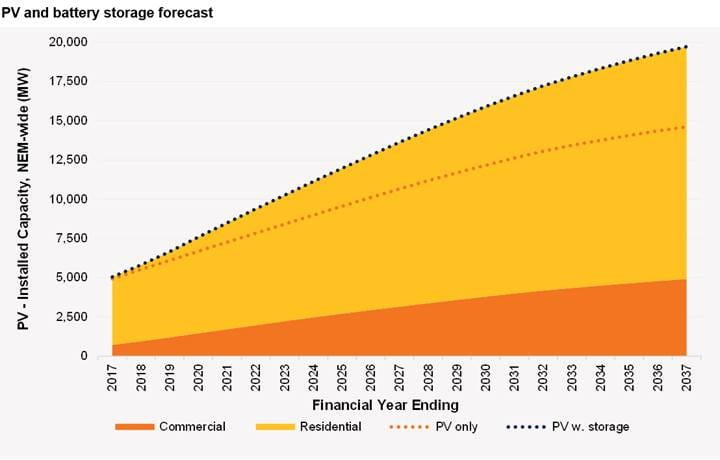

- Over the forecast horizon, installed rooftop photovoltaic (PV) capacity (including those which have attached battery systems) is forecast to continue growing, from around 5 gigawatts (GW) today to 19.7 GW by 2036–37. AEMO has assumed that it is technically feasible to integrate this amount of rooftop PV into the network over the forecast horizon, through a mix of market, network, and non-network (such as storage) solutions to address issues such as increasing variability in system demand, low daytime demand, and increased ramping at morning and afternoon electricity system peaks.

- Growth in installed PV is forecast to remain high initially, driven by consumers seeking to better manage their energy use, security, and costs. From 2019–20, the growth rate is forecast to slow, with federal incentives progressively being phased out, and the level of installations reaching saturation point due to availability of suitable roof space.

- Forecast growth rates are particularly high for commercial PV systems, and PV systems combined with battery storage.

- Battery storage installations are forecast to reach 5.6 GW by 2036–37, up from a capacity close to zero today. AEMO expects a proportion of new storage to be aggregated and used for price hedging by retailers and provision of ancillary services, further increasing the value streams from innovation and accelerating the rate of uptake.

- The forecast battery storage uptake is significantly faster than in the 2016 NEFR, and the capacity forecast to be installed to 2029–30 is double the capacity that was forecast last year. This change is driven by the projected costs of storage falling, and continuing to fall, faster than was assumed in 2016. Around 2029–30, growth is projected to reduce as the market is expected to start becoming saturated, with more than 2 GW of storage installed at the end of the period in 2036–37 than forecast in 2016.

- Strong scenario growth forecasts are stronger for both rooftop PV (23.6 GW of projected capacity by 2036–37, 20% more than in the Neutral scenario) and battery storage (6.8 GW installed by 2036–37, 22% above the Neutral scenario). The Weak scenario sees lower projected uptake of both technologies, with forecast rooftop PV installed capacity forecast to reach 17 GW by 2036–37 (14% lower than Neutral) and battery storage forecast to reach 4.8 GW (15% lower than Neutral).

- The projected impact of this forecast uptake on annual consumption is covered by the residential and business consumption pages, while the projected impact on maximum and minimum demand is covered on the maximum and minimum demand page.

Regional insights

Regional forecasts generally share the national trends, with minor differences as highlighted below.

New South Wales

New South Wales has strong forecast growth in rooftop PV uptake, and is projected to become the region with the largest installed capacity (7.6 GW) by 2036–37. This is mainly because this region has the highest number of projected connections, as the percentage of households with PV is forecast to remain lower than in some other regions. Strong growth of PV installations coupled with battery storage is forecast, especially after 2019–20, driven mainly by expected declining battery costs.

Queensland

Queensland is forecast to have continued steady uptake of rooftop PV installations until 2031–32, with growth in the commercial sector forecast to offset saturation being expected to be reached in some residential areas. After 2031–32, a rapid decline in annual installations is projected, as saturation is expected to be reached in most regions. By 2036–37, 5.1 GW of rooftop PV is forecast to be installed. The state already has a high penetration of rooftop PV, so (because the modelling does not consider retrofit of storage to existing systems) relatively low penetration of installations combined with storage is forecast.

South Australia

South Australia currently has the highest penetration of residential rooftop PV of all the NEM regions. As a result, the region is forecast to reach saturation earlier than most others, causing forecast growth to decline towards the end of the outlook period before reaching a total 2.1 GW of rooftop PV capacity by 2036–37. Some of the projected decline in residential growth is expected to be offset by a higher projected uptake of commercial PV systems.

Tasmania

Tasmania continues to have slower forecast growth of PV installations compared to the other regions, in both the residential and commercial segments, because lower insolation (sunshine) levels make systems less financially attractive. Only 250 megawatts (MW) of capacity is forecast to be installed by 2036–37.

Victoria

Residential PV uptake in Victoria is forecast to grow steadily until the mid-2020s. Projected uptake in the commercial sector remains steady across the outlook period, leading to a forecast total installed capacity of more than 4.3 GW by 2036–37.

Consultant Reports